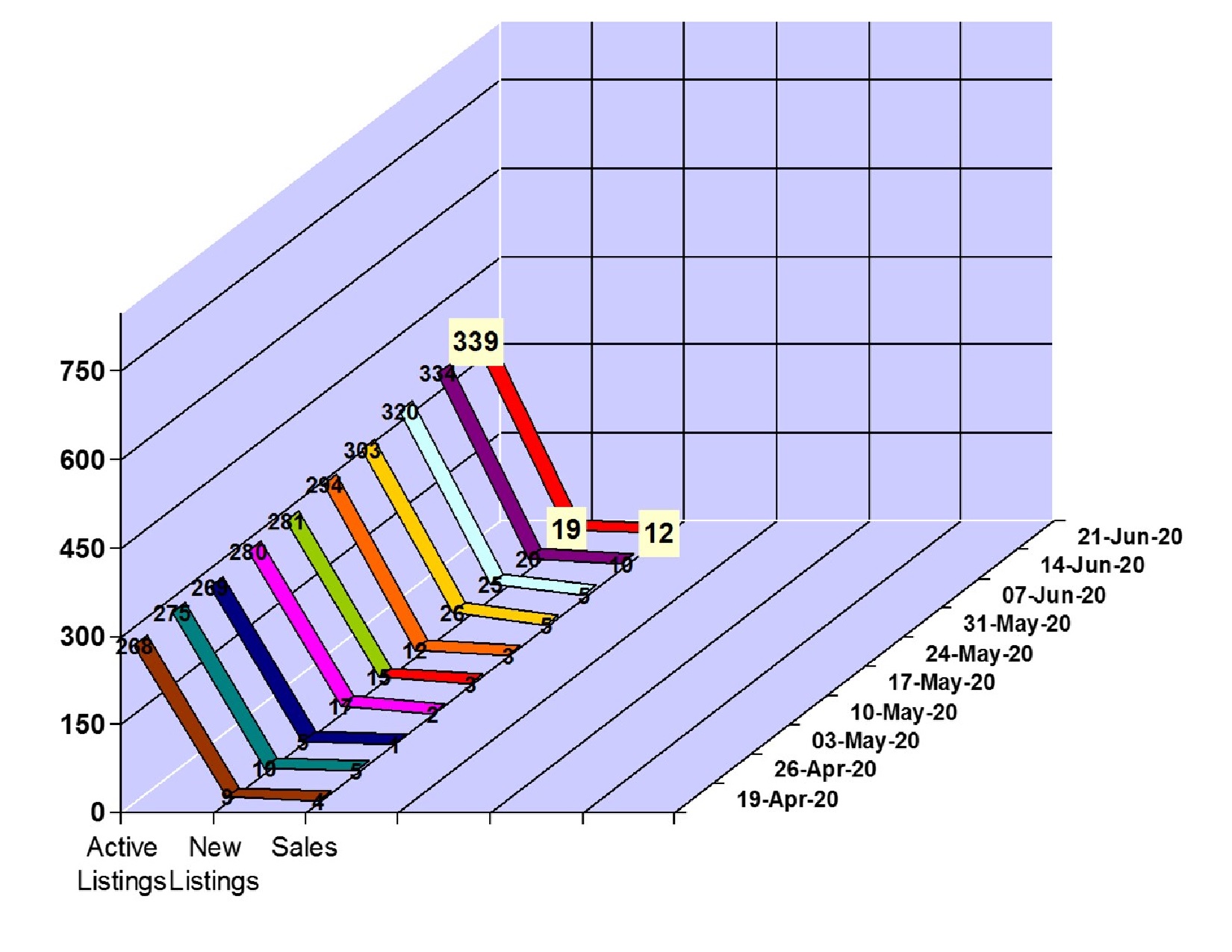

Whistler Real Estate | 5 Properties Sold

Sales for the Week of June 15 to 21, 2026

Whistler Condo Sales: 3

Price Range: $250,000 to $13,525,000

Whistler Townhouse Sales: 1

Price Range: $3,250,000

Whistler Chalet Sales: 1

Price Range: $2,160,000

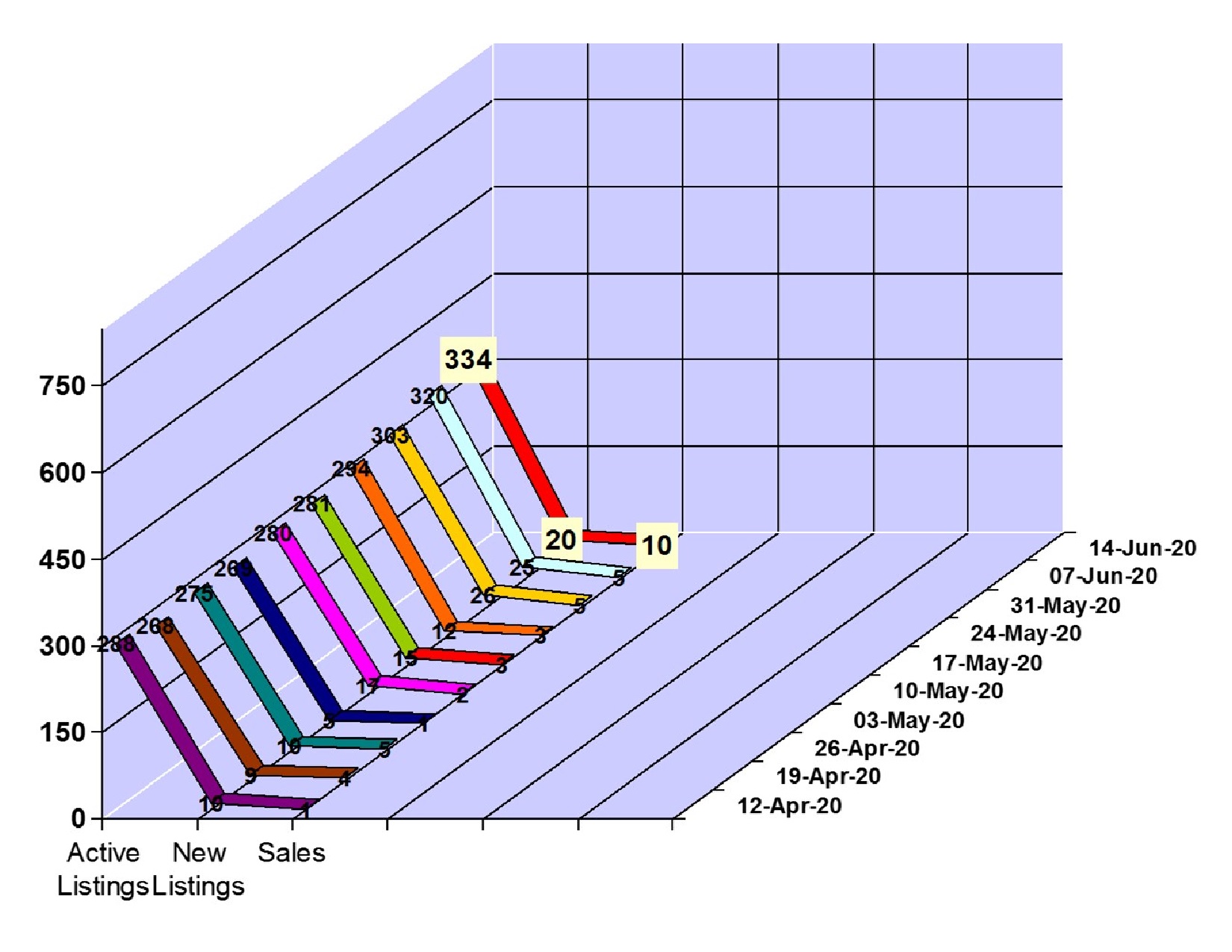

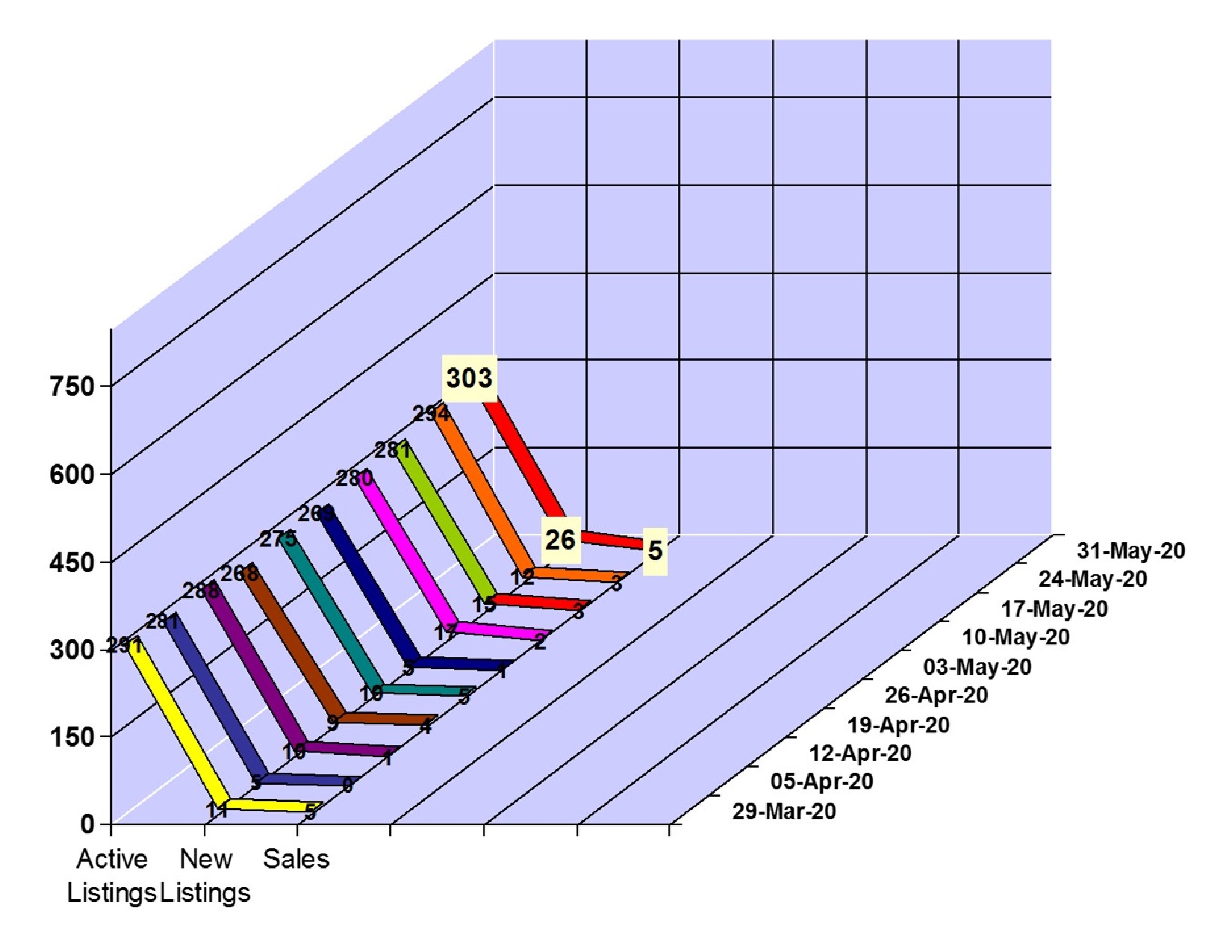

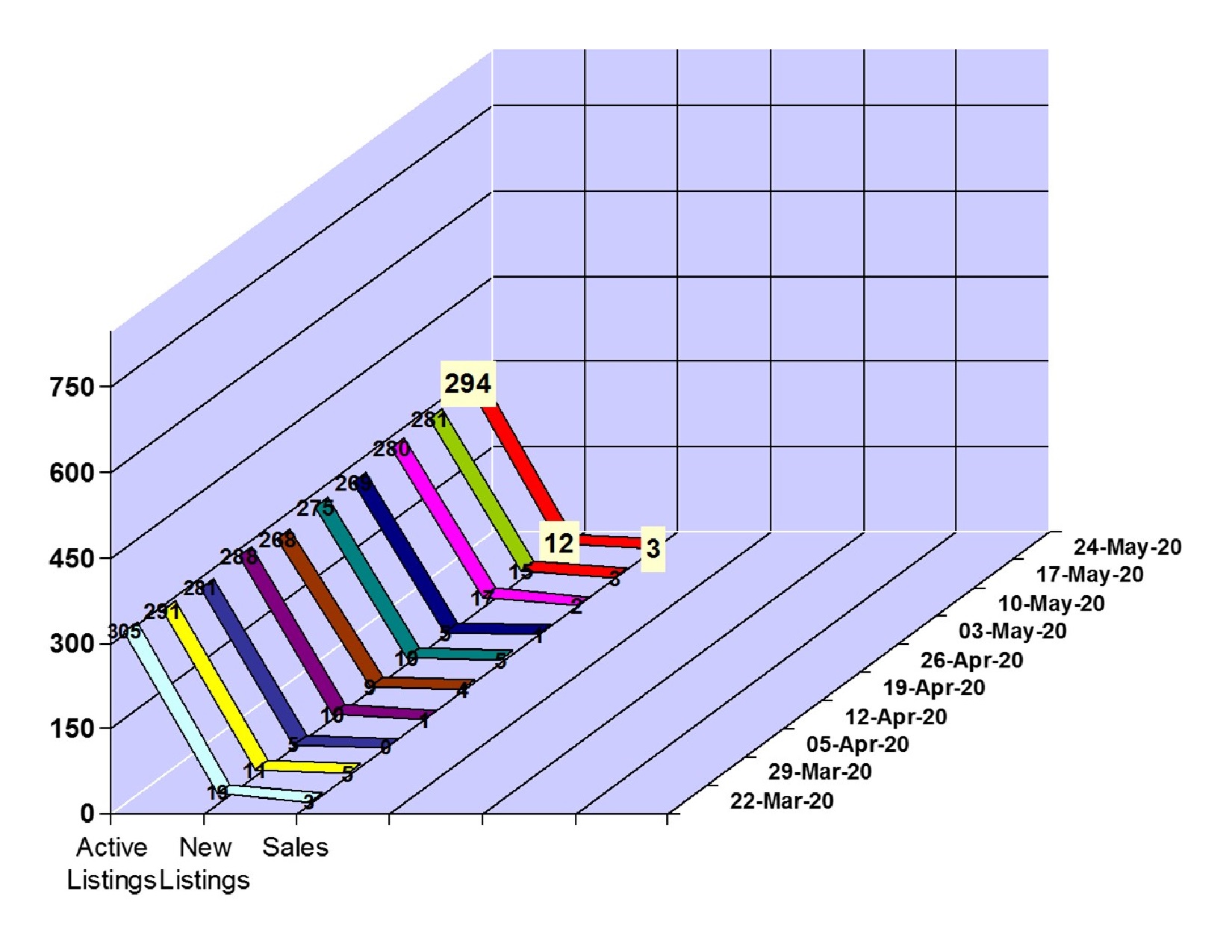

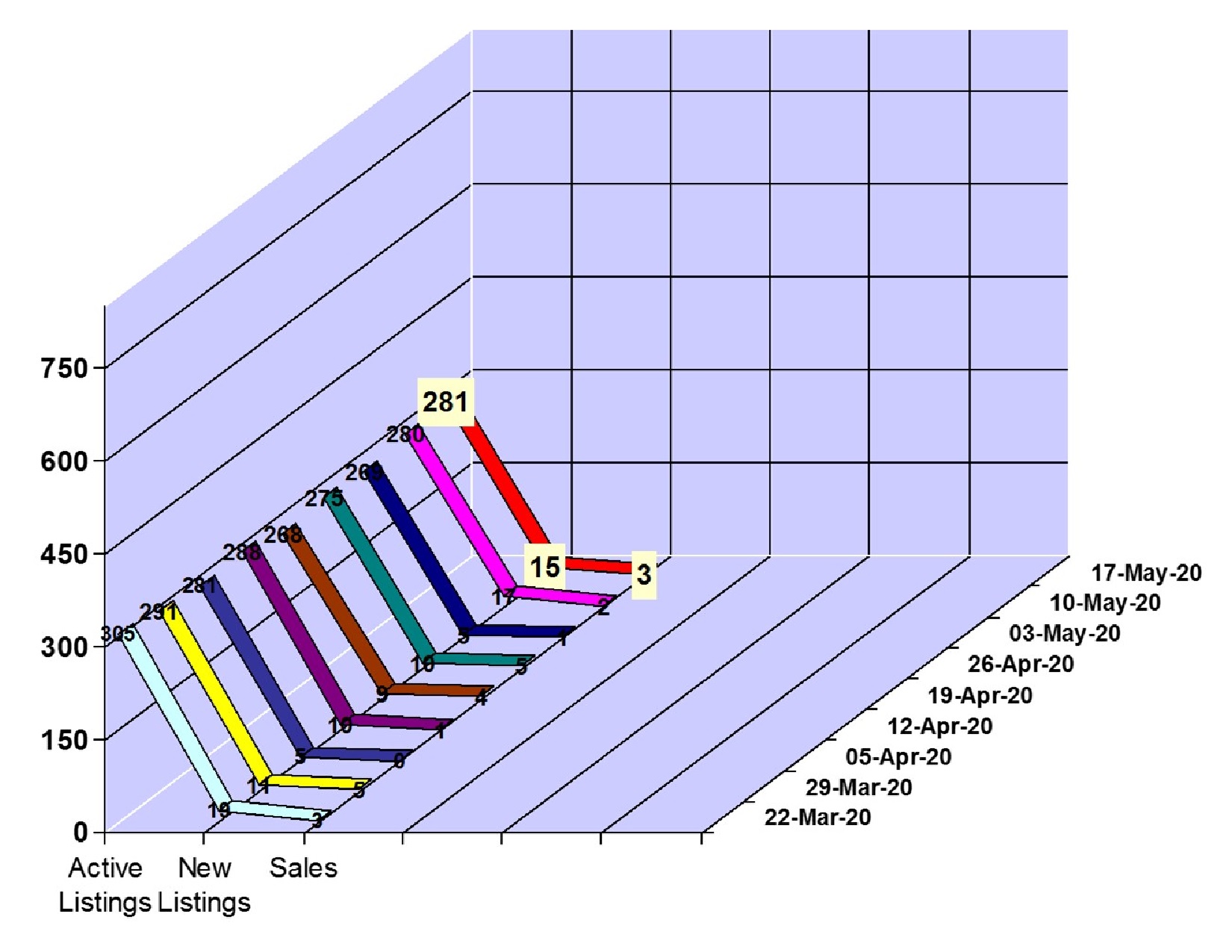

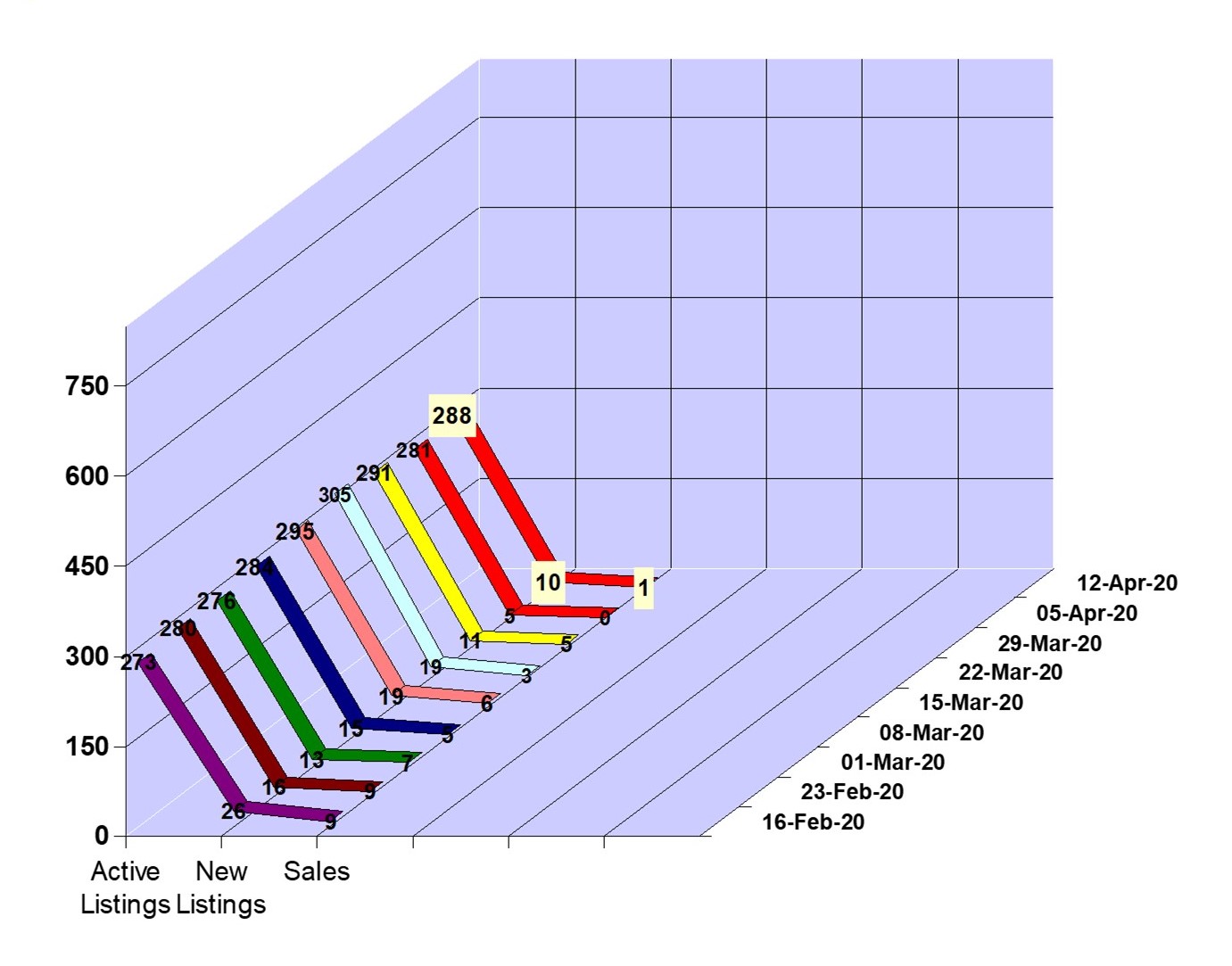

14 new property listings came on the Whistler real estate market. There are 281 active listings on the market.Click here to view the new listings for the week.