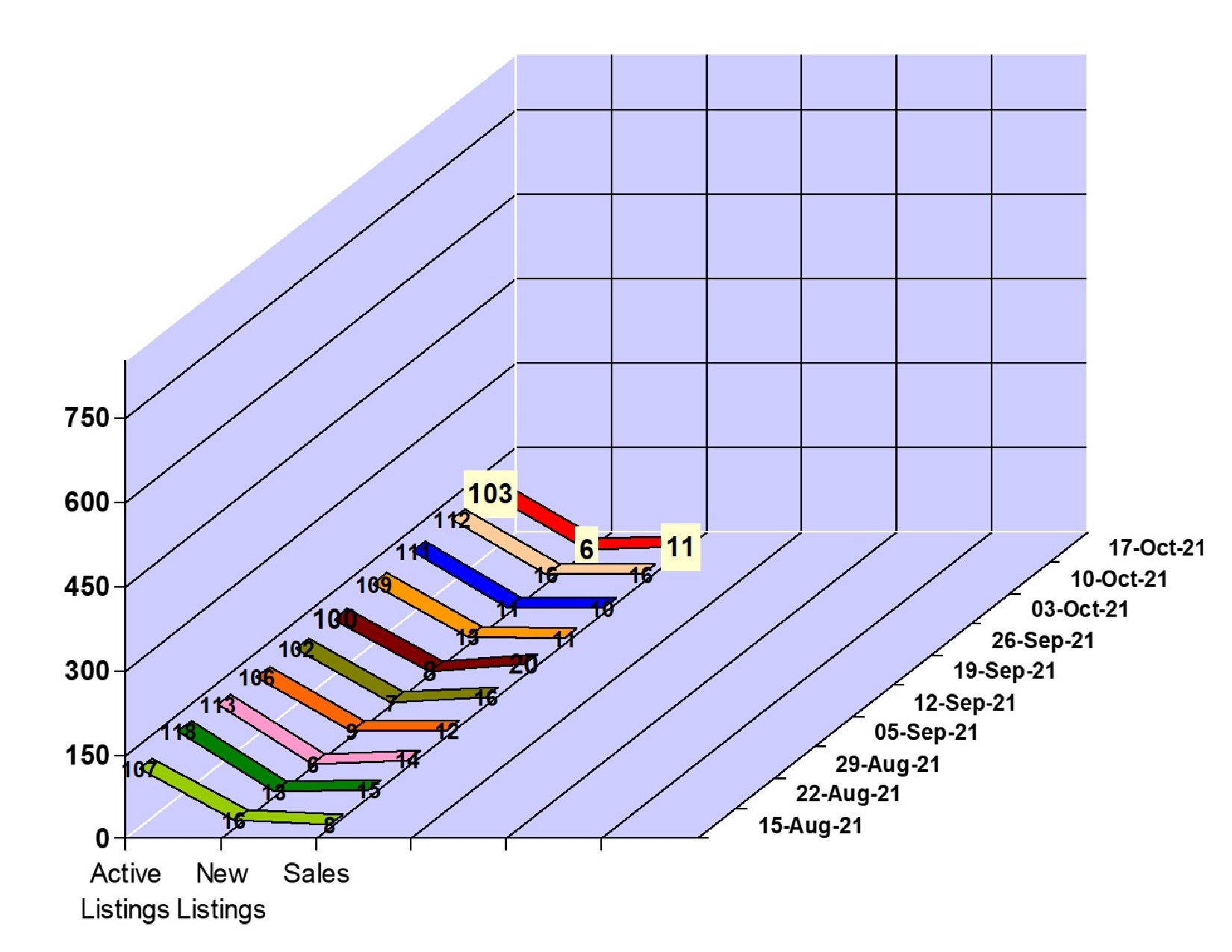

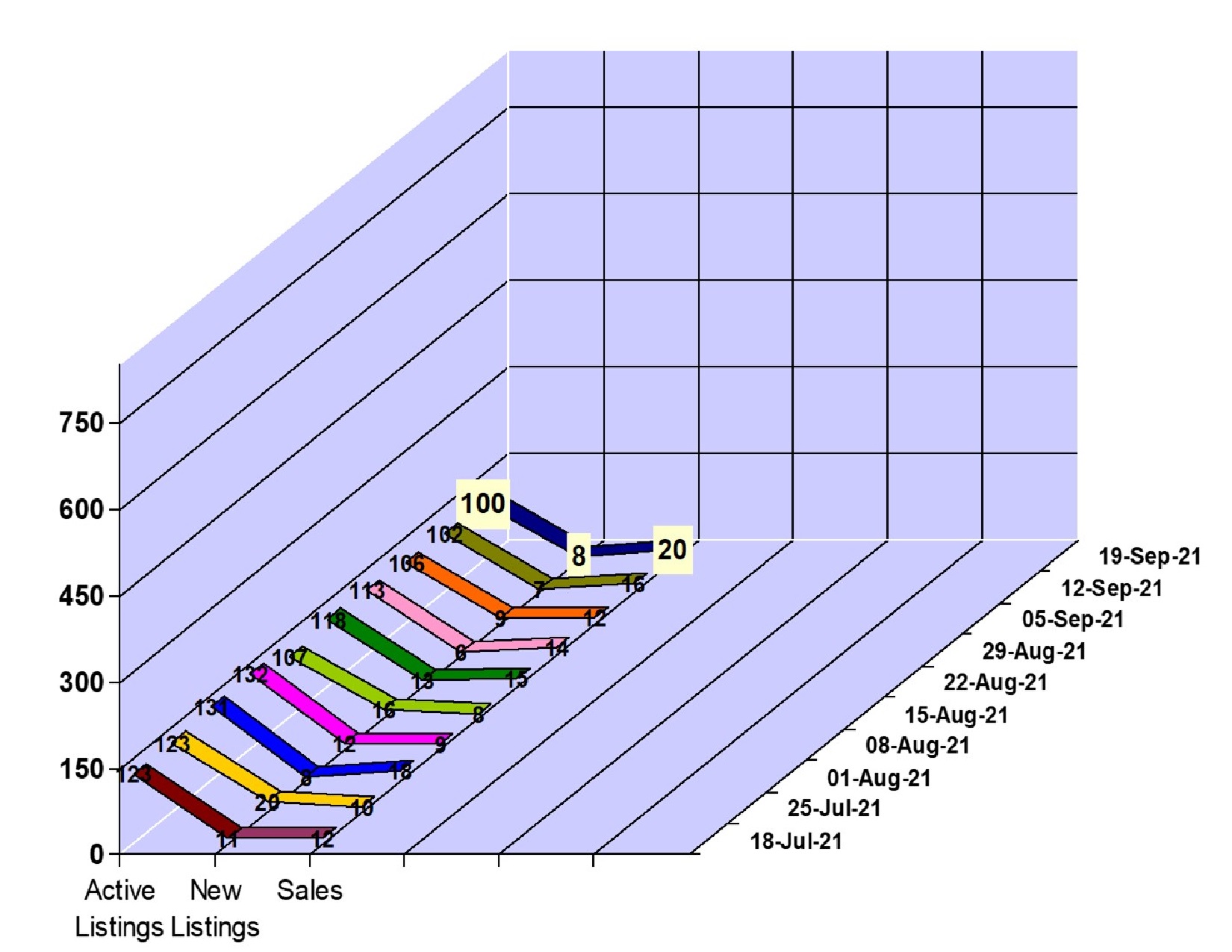

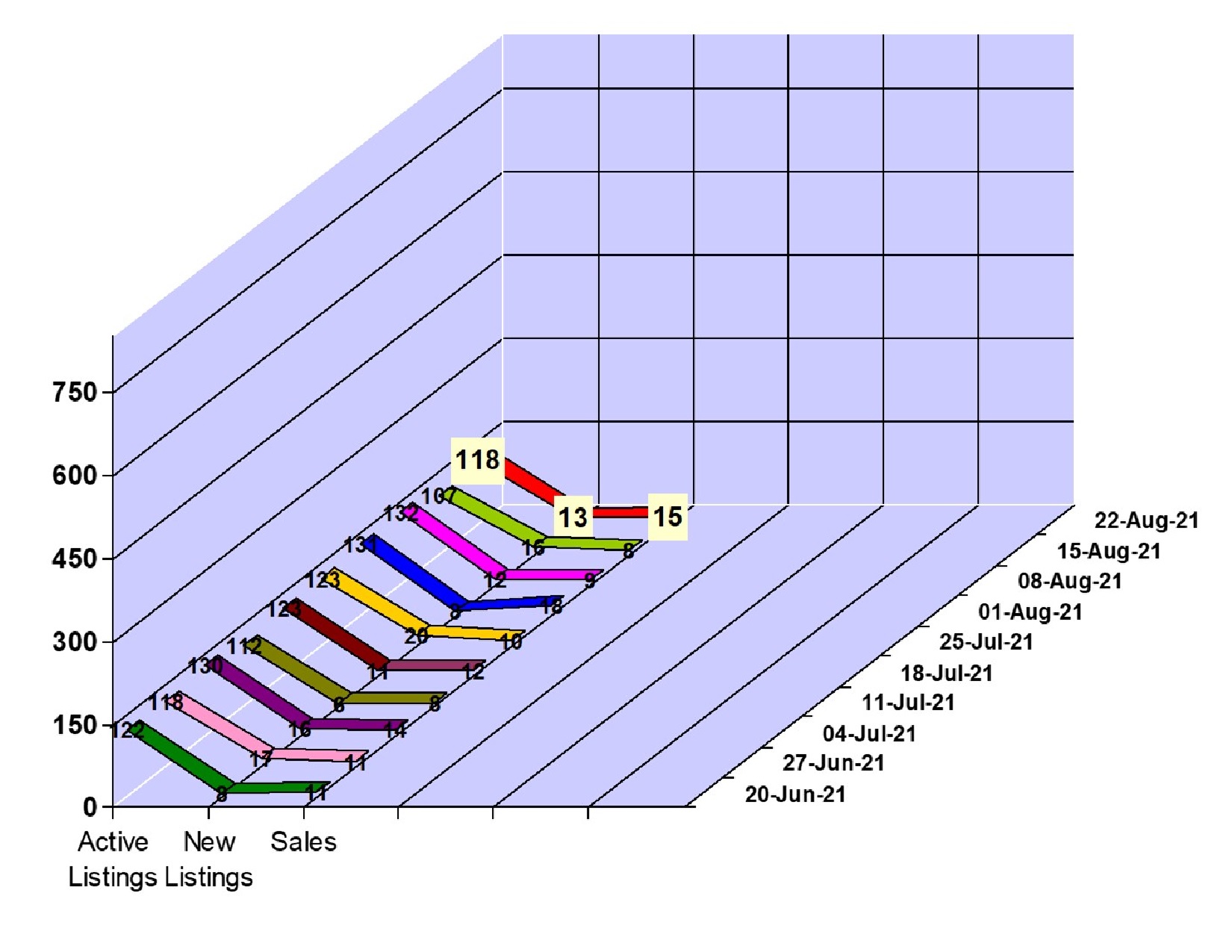

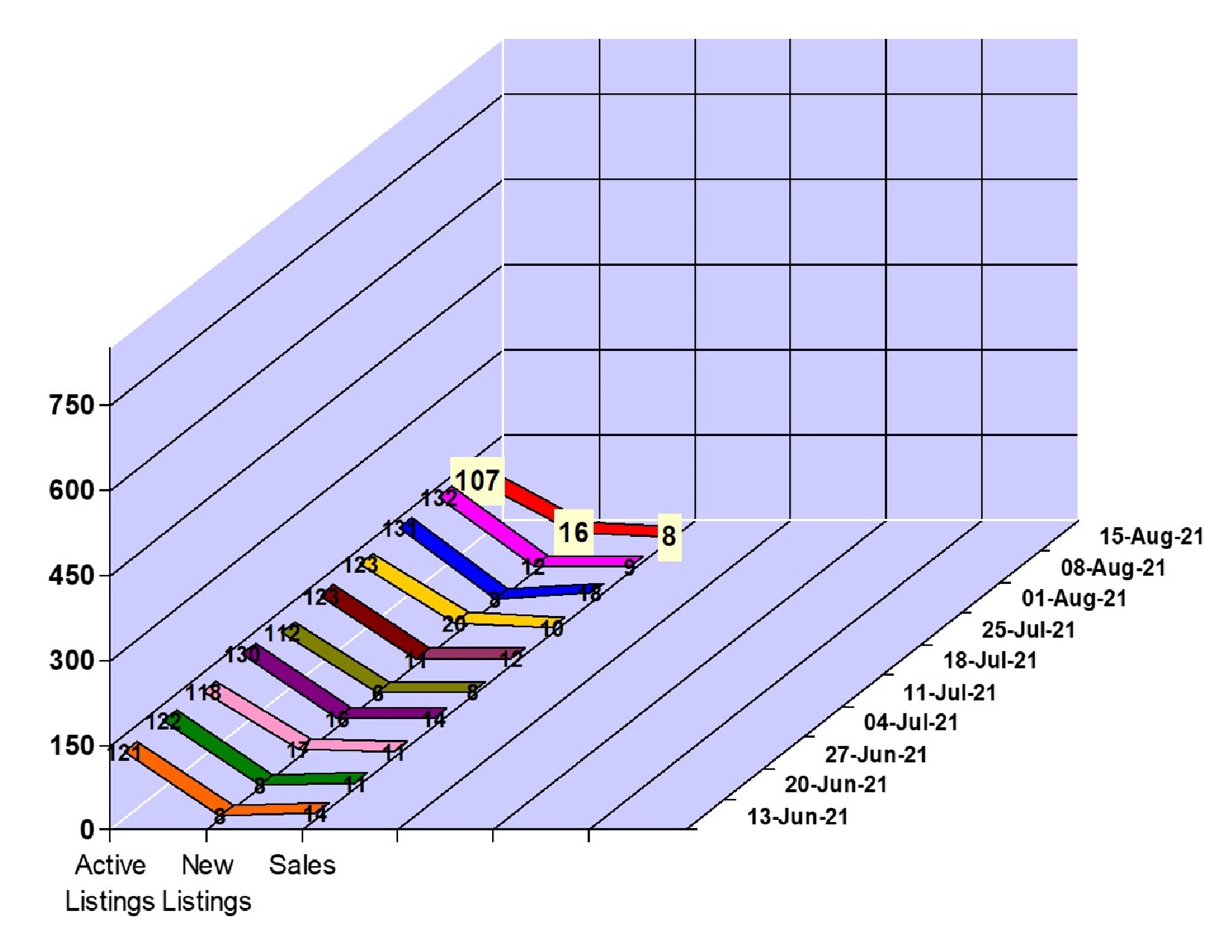

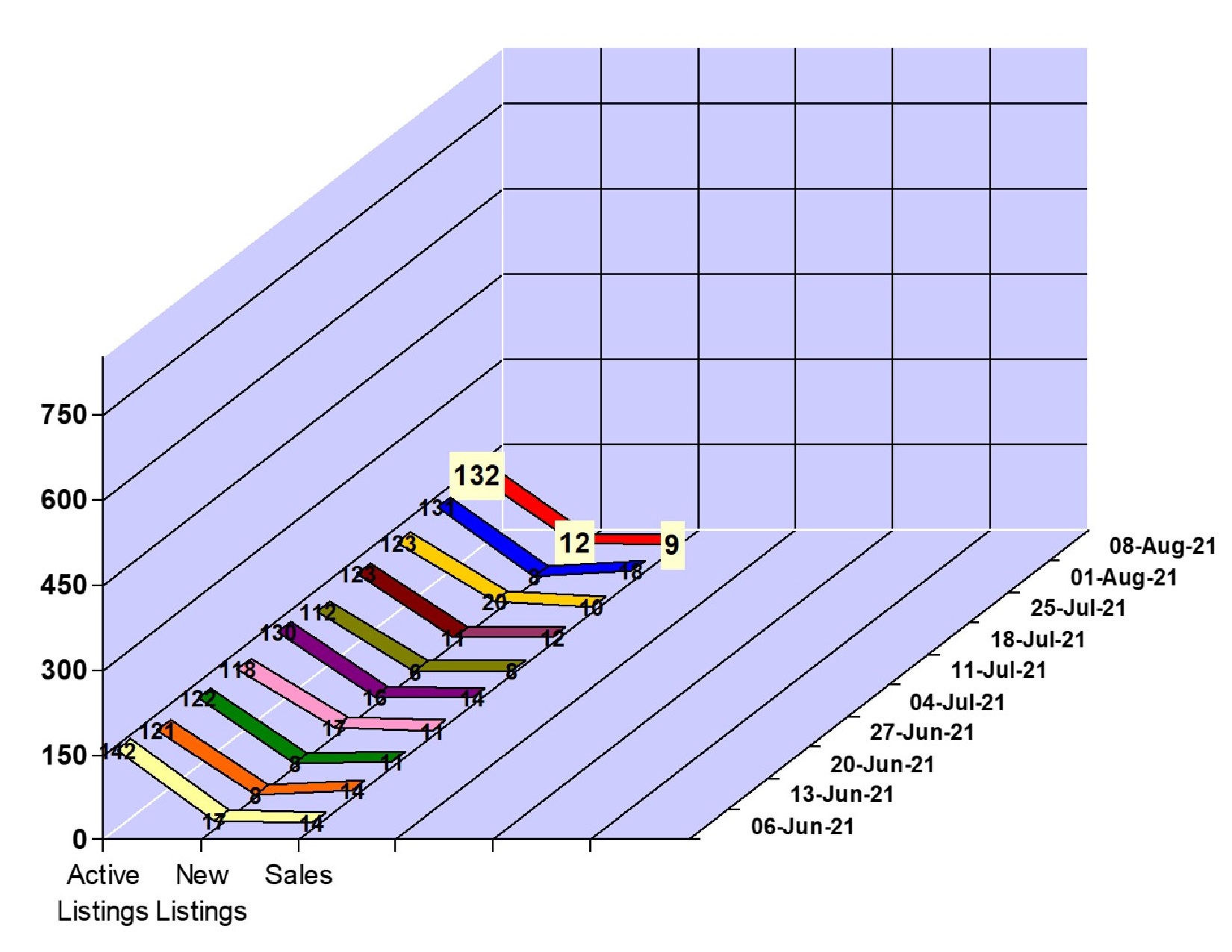

Whistler Real Estate | 11 Properties Sold

Sales for the Week of October 11 to 17, 2021

Whistler Chalet Sales: 2

Price Range: $2,095,000 to $2,550,000

Whistler Condo Sales: 3

Price Range: $1,518,000 to $1,545,000

Whistler Townhouse Sales: 4

Price Range: $1,049,000 to $1,660,000

Whistler Duplex Sales: 1

Price Range: $2,499,000

Whistler Vacant Land Sales: 1

Price Range: $1,225,000

6 new property listings came on the Whistler real estate market. There are 103 active listings on the market. Click here to view the new listings for the week.

Do you have questions about the Whistler real estate market, please contact me here directly with them.